In recent years, the way businesses process payments has drastically changed in this rapidly changing digital economy.

Along with the key innovations driving online payment processing, payment aggregators play a very important role.

With the beginning of growth for eCommerce, the demand for faultless and efficient ways of taking care of payments securely is ever on the rise.

The role of a payment aggregator plays an important role in making all that possible.

This lengthy guideline will take a closer look at what a payment aggregator is, how it works, its benefits, and how it differs from other kinds of payment solutions, such as payment gateways and payment facilitators.

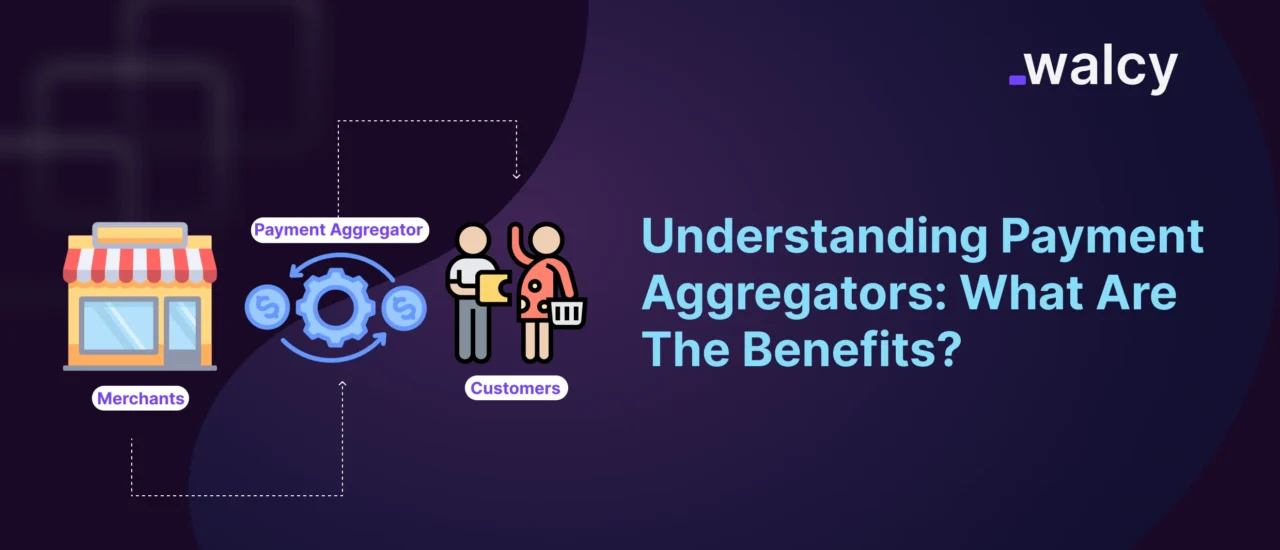

What is a Payment Aggregator?

A payment aggregator is a firm that enables companies to accept many digital payment methods through a single system without having to establish separate bank or processor connections.

By serving as a middleman between the merchant and their client, the aggregators enable the company to accept a variety of payment methods, including bank transfers, digital wallets, credit/debit cards, and even cryptocurrencies.

In essence, payment aggregators integrate different ways of processing payments without requiring the merchants to open different merchant accounts with banks or any payment processors.

It can also be called the merchant payment system as it enables the merchants to efficiently, safely, and at a meager cost process the payment transactions of customers.

How Does a Payment Aggregator Work?

At its core, how a payment aggregator works is relatively simple in form but seldom more effective. Here’s a step-by-step breakdown of the key stages:

Step 1:

In regular cases, the merchant simply online sign-up themselves with a payment aggregator.

They are not required to open any dedicated merchant account with any bank.

The aggregator shall take care of all the technical and regulatory requirements needed for processing the payments.

Step 2:

If the customer is to make any transaction, say on an online store, the request for payment goes to the payment aggregator.

Step 3:

The aggregator of the payment would then gather the details about the mode of payment chosen by the customer.

For instance, details related to a credit card – and transfer them to the concerned financial institution or payment processor – such as Visa, MasterCard, PayPal, etc. – for authorization.

Step 4:

The financial institution or the processor of the transaction verifies whether the payment is valid and the available account balance is adequate to support the payment.

If the payment is authorized, the account of the customer is then deducted accordingly.

Step 5:

The aggregator receives the funds that are collected from the payment processor, pools them together, and transfers them to the merchant’s account after deducting the service fees.

Step 6:

Quite often, aggregators will provide detailed reports and dashboards for merchants for them to track their transactions, and performance of their payments, and reconcile their accounts.

Payment Aggregator – Key Benefits

-

Easy Integration of Online Payments

Integrate online payments, which are always complex and resource-intensive for any business.

This is made easy by the payment aggregators while providing plug-and-play solutions that can easily integrate with the online store or application.

Whatever the size of your business, big or small, aggregators have simple and easy options to integrate them without requiring deep technical know-how.

-

Cost-Effective

Payment aggregators are generally cheaper in pricing than traditional payment processing.

This is because it consolidates several merchants’ processing power onto one shared infrastructure, which enhances the reduction of overhead costs on the part of each business.

That is very helpful, especially to small businesses or startups, since this provides them with an opportunity to accept payments without needing high set-up or running costs.

Read about: International Payment Fees | The Essential guide.

-

Threat-free processing

In today’s world, cybersecurity threats continue to rise, and hence security in payment processing is paramount.

Typically, payment aggregators are enabled with robust encryption methods, fraud detection, and compliance with international standards of security, including PCI-DSS.

This will help in the protection of sensitive information of customers at every transaction and will build trust among consumers.

You shall love to read: Online Payment Security: Best Practices to Keep Your Transactions Safe

-

Multi-Currency Payment Solutions

The capacity to process payments in several currencies is crucial for any firm that operates worldwide.

Multi-currency payment solutions are supported by payment aggregators, which may help a merchant receive payments from customers across the world. Further, this can extend the reach of an online store, mostly in regions where credit cards or local payment methods are the means of transaction.

Read about: Best Multicurrency Account: What Is It And How It Works?

-

Faster Settlement and Payouts

These payment aggregators thus allow for speedy processing of payouts, increasing the timeframe within which a merchant will have received their money from a particular transaction.

This is essential in cash flow management, especially for small businesses or e-commerce platforms that seek to plow the money back into inventory, marketing, or operations.

Read about: What is Payment Settlement? How does it Work?

Payment Aggregator vs. Payment Gateway

Probably the most common misunderstanding has to do with the difference between a payment aggregator and a payment gateway.

While these are very closely related, the functions they play within the ecosystem of online payments differ.

- Payment Gateway

It is a technology that enables the passing of payment information amongst the customer, merchant, and payment processor.

It is intended to move the data of the transaction to financial institutions for approval and then send the response to the merchant on the back end.

The payment gateways can enable merchants to take payments online but do not handle settlement or merchant account services.

- Aggregator

An aggregator consolidates the complete payment process- merchant account, payment processing, and transaction settlement.

Like a merchant payment system, it takes responsibility for everything from transaction initiation to final settlement.

While the payment gateway has to do with safe transaction processing, the payment aggregator provides an all-in-one solution, comprising among others, the services of a payment gateway, added value fraud prevention, multi-currency support, and merchant accounts.

Payment Facilitator vs. Payment Aggregator

There are several subtle differences between a payment aggregator and a payment facilitator.

Both are third-party entities that allow different merchants to accept various forms of payments without having an individual merchant account with any financial institution, but the key difference lies in their operational structure.

- Payment Facilitator:

The payment facilitator is the more comprehensive solution whereby the direct underwriting of merchant accounts is performed.

It onboarded the quick business to process the payments under the payment facilitator master account.

PayFac is responsible for compliance underwriting and settlement for their sub-merchants.

Essentially, the PayFac stands in between the middleman of the merchant and the payment processor.

Each sub-merchant is considered an extension of the facilitator’s account.

- Payment Aggregator

In direct contrast, a payment aggregator does not normally provide a merchant with a unique merchant account through which to receive payments.

A merchant aggregator consolidates different merchants’ payments and settles those payments under one master account.

The simple function of facilitating the process of payment without managing or underwriting merchant accounts describes an aggregator.

While both models allow merchants to receive payments without requiring their own merchant accounts, a payment facilitator model usually takes a bit more responsibility and risk compared to a payment aggregator.

Top Payment Aggregator Companies

Among the top-rated payment aggregator companies that have been recognized for offering smooth solutions are:

- Stripe

Stripe is probably the most famous payment aggregator, delivering a powerful toolkit for each business in the sphere of payment processing, subscriptions, invoicing, and financial reporting. Most modern startups, technology companies, and e-commerce websites rate Stripe as the friendliest to users and developers.

- PayPal

PayPal was one of the pioneers and market leaders in online payment processing. By allowing aggregation of payments, businesses of all sizes could receive payments via their portal, trusted by millions worldwide.

- Square

Square is another major player, especially in the point-of-sale and mobile phone payment processing market. Square has made it easy to integrate payments for both physical stores and online retailers, hence becoming universally applicable to businesses of any kind.

- Adyen

Adyen is a global payment aggregator offering multi-currency payment processing, known to cater to large enterprises with very complex needs.

This company provides end-to-end online, mobile, and in-store payment solutions

Conclusion

In the payment processing space, a payment aggregator will fall under an essential service for any business looking to manage online transactions in as non-complicated, secure, and cost-effective manner as possible.

While acting as a one-stop solution for the integration, processing, and settlement of payments, the payment aggregator makes it rather easy for the merchant to attend to growing his business rather than manage complex payment systems.

Since the rate of digital payments is continuing to increase globally, it also means that a good payment aggregator has increased importance in the world.

However, for a small online retailer or any multinational company with a storefront, or even at a startup, using payment aggregators makes operations seamless and smoothies customer experiences.

Read about: All About Overseas Payments (2024); Comprehensive Guide

Do follow us on Facebook and LinkedIn, to stay connected with us.